Author: Frank, PANews

How difficult is it to find a profitable "golden key" in prediction markets?

On social media, you often see many people claiming to have discovered a secret to smart money's profitability, but in reality, they provide no substantive information. What people can see is only the growing profit curve of these funds, not the underlying logic.

So, how can one build a personalized trading strategy suitable for prediction markets?

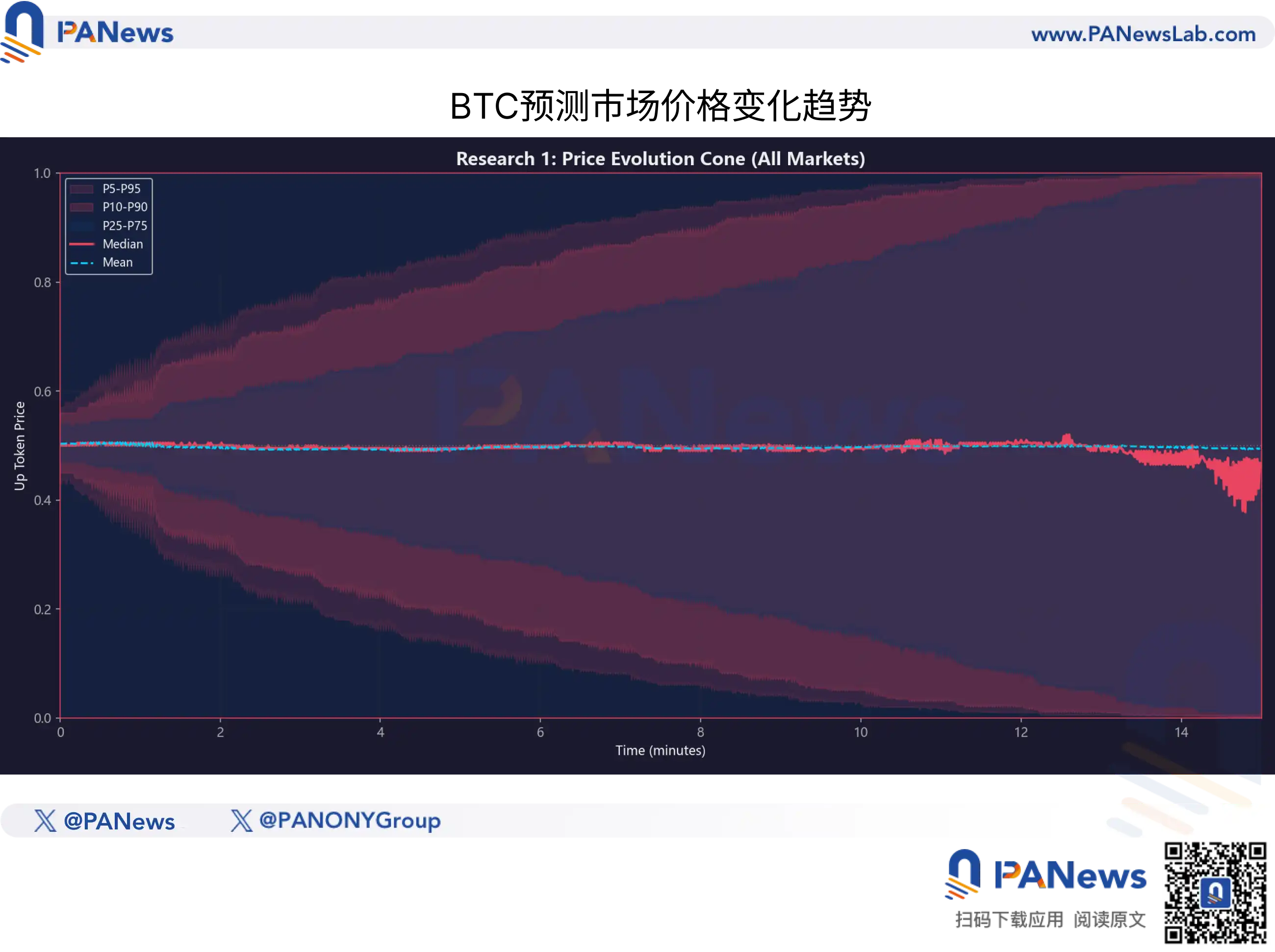

PANews took the BTC 15-minute prediction market as an example, analyzing nearly 27.73 million transactions and 3,082 window periods over the past month, arriving at some conclusions that may defy conventional wisdom. In a previous article, we already conducted a macro-level analysis of this market. This time, we will delve deeper to find that potentially existing "golden key."

Shattered Illusion: The Complete Failure of K-Line Technical Analysis

Have you ever considered a strategy that treats prediction markets like stocks or cryptocurrencies, analyzing entry and exit points purely based on price movements, combined with position management, stop-loss, and take-profit elements, to create a trading strategy entirely detached from BTC's行情, focusing solely on the price changes in prediction markets?

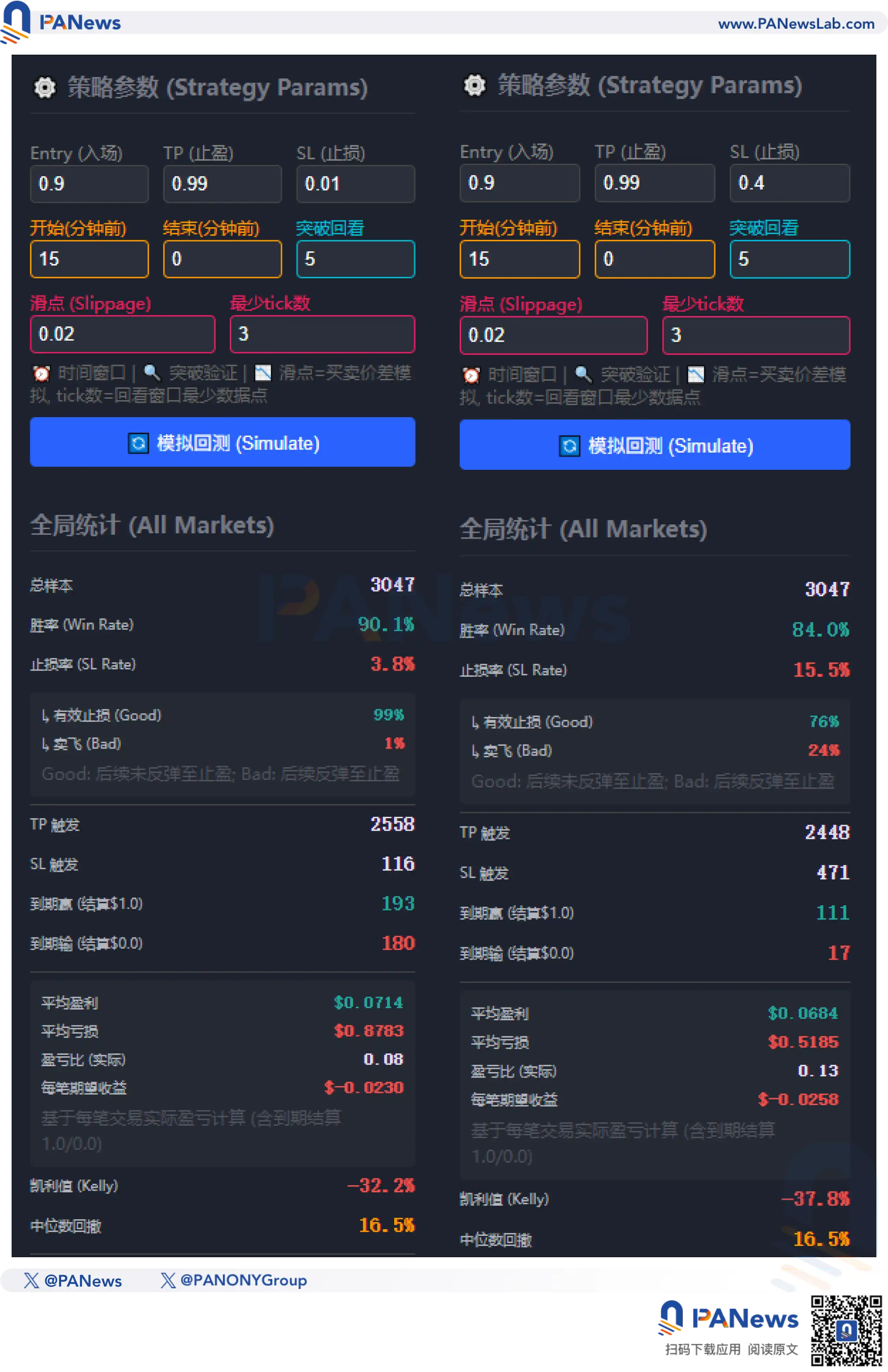

In traditional crypto markets, this approach is known as the "technical analysis" school. In theory, this should work equally well in prediction markets. Therefore, PANews also conducted simulations in this direction and developed a custom prediction market backtesting system. This system can input factors such as entry points, take-profit points, stop-loss points, entry timing, and exclusion of干扰 prices to calculate the actual profit-loss ratio, win rate, and other elements of the strategy from over 3,000 markets in the past 30 days.

Initially, with incomplete data (Polymarket's historical data only provides 3,500 entries per market), the backtest results could easily find profitable answers. For example, entering at 60%, selling at 90%, stopping loss at 40%, and setting a certain window period for trading.

However, the actual test results were vastly different. Under real execution, the profit curve of this strategy slowly declined like a钝刀割肉 (dull knife cutting flesh). So, we tried to补全 the data as much as possible. After trying various methods, we finally obtained the complete price information data for all markets. This time, the results finally began to align with reality.

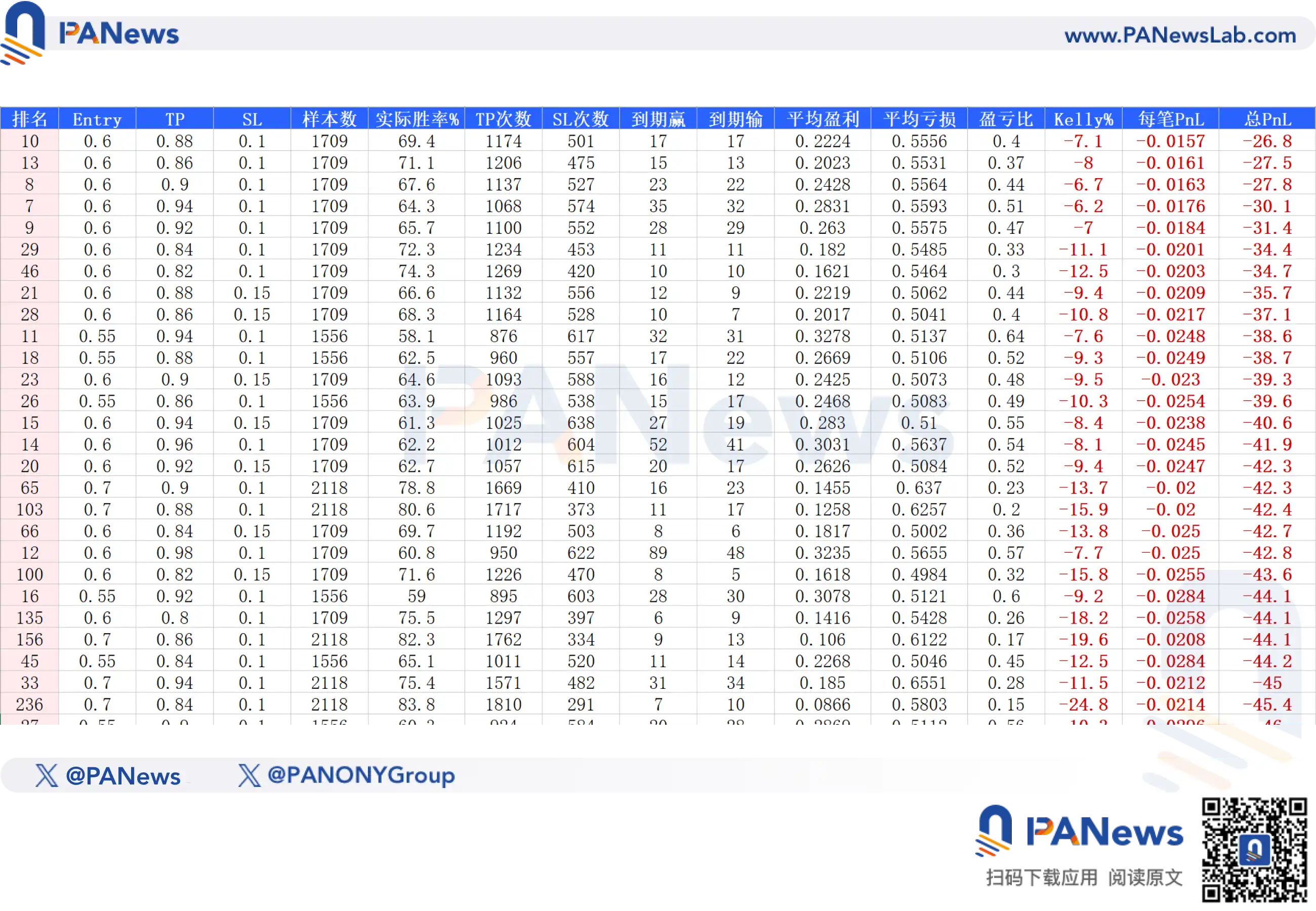

In real data testing, PANews simulated 690 combinations of factors including price, take-profit/stop-loss, entry timing, interference exclusion, and slippage. The final result was that not a single strategy could achieve a positive expected return.

Even the highest possible return had an expected value of -26.8. This result indicates that in prediction markets, any purely mathematical prediction that excludes the event itself has almost no possibility of profitability.

For example, the much-discussed "end-of-market strategy" on social media involves buying at 90% and selling at 99%. It seems this strategy would have a very high win rate and be profitable in the long run. From the actual test results, this strategy indeed has a high win rate of 90.1%, achieving take-profit in 2,558 out of 3,047 simulations. However, the terrifying part is that under this strategy, the actual profit-loss ratio is only 0.08, and the final expectation given by the Kelly criterion is -32.2%, making it not worth adopting.

Some might say, would adding a stop-loss improve the profit-loss ratio? But the残酷的现实 (harsh reality) is that while the profit-loss ratio might improve, the win rate correspondingly decreases. For example, setting a stop-loss at 40% reduces the win rate to 84%. Combined with the still low profit-loss ratio, the final Kelly expectation is -37.8%, still a loss.

Conversely, the strategy closest to profitability was buying for a reversal—buying at 1%, betting that the market would reverse and ultimately win. In the simulation, this approach had a win rate of about 1.1%, higher than the price probability, and an extremely high profit-loss ratio of 94, resulting in an expected return of 0.0004. However, this前提 (precondition) assumes no slippage or transaction fees. Once fees are considered, it instantly becomes a negative expectation.

In summary, our research in this area found that in prediction markets, relying solely on technical analysis from financial trading cannot achieve profitability.

The Trap of "Two-Way Arbitrage"

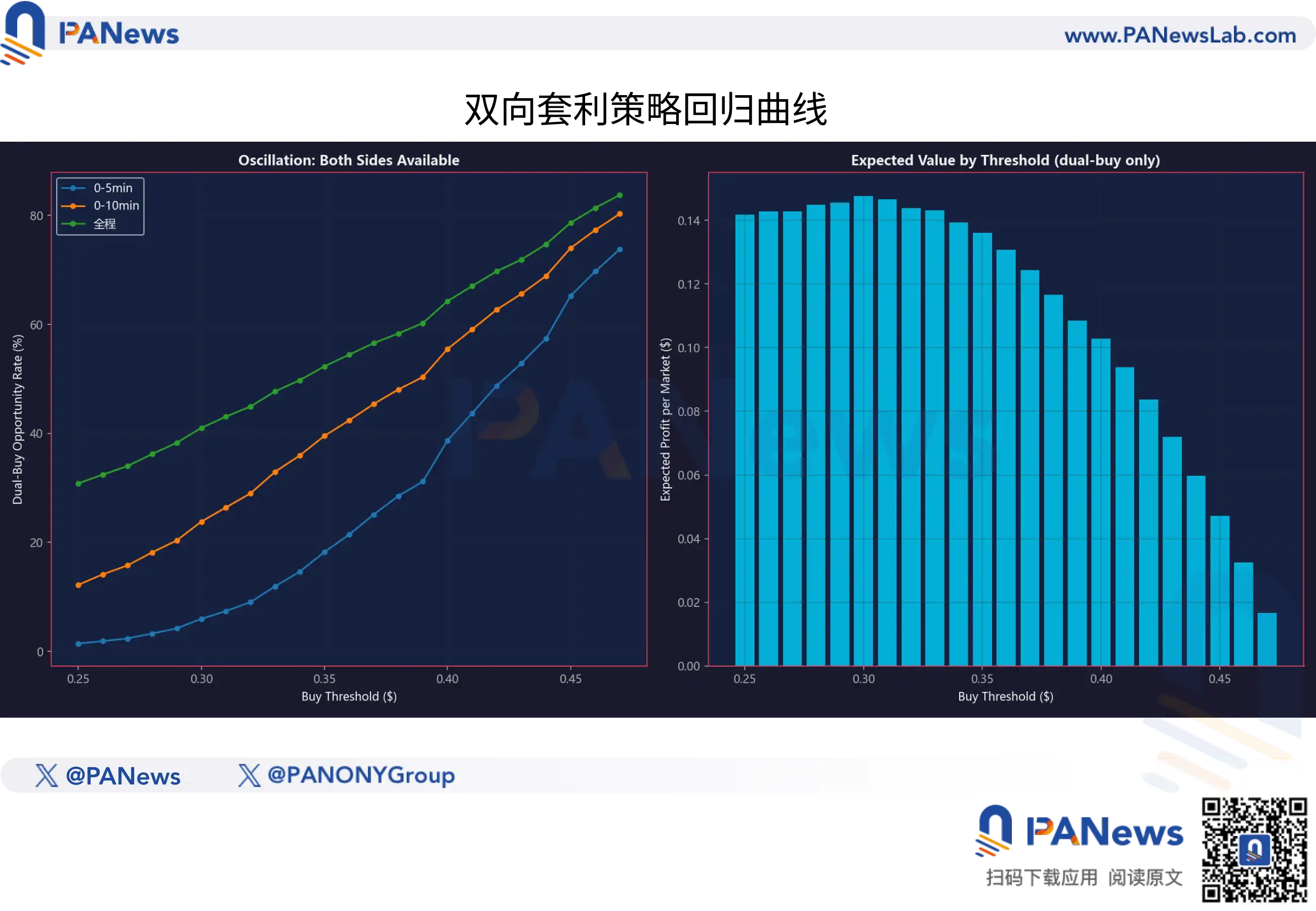

So, besides this approach, there's another mainstream view: two-way arbitrage. The idea is that if the total cost of YES + NO is less than 1, you can profit regardless of the outcome. Again, this is an idea that is丰满 (plump) in theory but骨感 (bony) in reality.

nFirst, if you opt for cross-platform arbitrage, there are already many bots doing this. Ordinary users simply cannot compete with bots for the meager liquidity.

So, to achieve this effect, another方案 (scenario) is, for example, in the same market, buying when the YES price drops to 40% and the NO price also drops to 40%, which could theoretically create a 20% arbitrage space.

But the final data results tell a different story. Although this strategy has a 64.3% win rate, its excessively low profit-loss ratio still leads to a negative expectation.

This "two-way strategy" looks beautiful on paper but is很容易翻车 (very easy to fail) in practice. Moreover, categorically, this strategy also falls under pure theoretical assumptions detached from the actual event changes.

Fair Value and Deviation Models are the "Golden Key"

So, what kind of strategy can truly achieve profitability?

The answer lies in the "time差" (difference) between the BTC spot price and the prediction market token price.

PANews discovered that the liquidity providers and market maker algorithms in prediction markets are not perfect. When BTC experiences sharp movements within a short time (e.g., 1-3 minutes), such as a sudden price jump exceeding $150 or $200, the price of prediction market tokens does not instantly "teleport" to the theoretical price.

Data shows that this "efficiency gap" in pricing takes an average of about 30 seconds to decay from its maximum value (approx. 0.10) to half (approx. 0.05).

Thirty seconds is an eternity for high-frequency trading, but for manual traders, it's a fleeting "golden window."

This means the prediction market is not a completely efficient market. It's more like a sluggish giant that often reacts half a beat slower after BTC's baton has already been waved.

However, this doesn't mean that fast hands can easily pick up money. Our data further shows that this "delay arbitrage" space is being rapidly compressed. In the微小波动区间 (tiny fluctuation range) where BTC moves less than $50, after deducting Gas fees and slippage, most so-called "arbitrage opportunities" are actually traps with negative expectations.

Besides momentum trading relying on speed, PANews' research also revealed another盈利逻辑 (profit logic) based on "value investing."

In prediction markets, "price" does not equal "value." To quantify this, PANews built a "Fair Value Model" based on 920,000 historical snapshots. This model does not rely on market sentiment but calculates the theoretical probability of winning for the current token based on BTC's current volatility state and the remaining time to settlement.

By comparing the theoretical fair value with the actual market price, we discovered the nonlinear characteristics of pricing efficiency in prediction markets.

1. The Magic of Time

Many retail traders intuitively believe that price should regress linearly over time. But data shows that deterministic convergence is accelerated.

For example, under the same BTC volatility conditions, the price correction speed in the last 3-5 minutes of a match is much faster than in the first 5 minutes. However, the market often underestimates this convergence speed, leading to frequent situations where token prices are significantly lower than their fair value during the mid-to-late stages of a match (remaining 7-10 minutes interval).

2. Only "Deep Discounts" Are Worth Buying

This is the most important risk control conclusion from this research.

Backtesting different levels of deviation index (Fair Value - Actual Price) found:

When the market price is higher than the fair value (i.e., buying at a premium), regardless of BTC's trend, the long-term expected value (EV) is negative across the board.

Only when the deviation index > 0.10, meaning the actual price is at least 10 cents lower than the fair value, does the trade have a robust positive mathematical expectation.

This means that for smart money, a price of $0.70 does not mean "a 70% probability of winning"; it is merely a quote. Only when the model calculates the underlying true win probability to be as high as 85% does $0.70 become a "bargain" worth betting on.

This also explains why many retail traders容易亏损 (easily lose money) in prediction markets—because your actual transaction price is likely bought at a level higher than the market's fair value.

For ordinary participants, this research is a sobering dissuasion and an advanced guide. It tells us:

Abandon K-Line Superstition: Do not try to find patterns in the price charts of prediction tokens; it's a mirage.

Focus on the Underlying Asset: Watch BTC's movements, not the prediction market盘口 (ticker).

Respect the Odds: Even with a 90% win rate, if the price is too expensive (premium), it is still a注定亏损的买卖 (sure-loss trade).

In this algorithm-dominated jungle, if ordinary retail traders cannot establish a mathematical coordinate system for "fair value" and lack the technical ability to capture the "30-second lag," then every click of "Buy" might just be a donation to the liquidity pool.